Hot Dog for Breakfast? What We Actually Know About the Polish Morning Shopper

LinkedIn

LinkedIn

1 in 10 children going to school buys a hot dog for breakfast. Not as an exception — as part of their morning routine.

Results from a study of Polish breakfast habits, conducted among people purchasing breakfast products, show that the “breakfast hot dog” is just one of several findings that contradict intuition.

Another one? Morning rush is not the exclusive domain of the young. The most time-pressed group in the morning are Poles over 50 — though it is younger people who more often actually eat breakfast on the go. In other words: the sense of morning pressure increases with age, but it does not necessarily translate into a greater tendency to buy breakfast on the go.

Below we look at what is actually happening during the morning purchase mission in Poland — and what it means for brands that want to be part of that everyday moment.

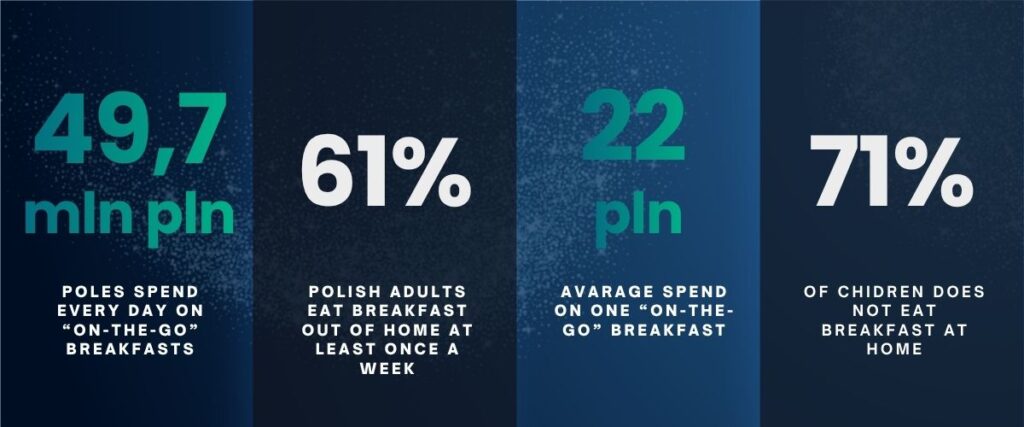

Scale: PLN 49.7M Daily and a Growing Market

Before the generational breakdown — the numbers, because they change the perspective.e.

Children are not abandoning breakfast — moving the shared meal „on the go”

One in four children never eats breakfast with their parents. Among primary school children in grades 1–3, only 28% do so every day; among secondary school students, just 17%.

This does not mean that parents are stepping out of the morning routine. Two thirds of breakfasts eaten outside the home are prepared in advance by adults. Mornings are still organized by parents — only the place of eating is shifting.

For brands this means children’s breakfast outside the home is often a planned mission, not simply an impulse purchase. The school route becomes an important purchase and consumption context — a place where the need is already present and the decision can be completed.

Autonomy as category driver for youngsters

Age differences in independent breakfast purchasing point clearly to a category trajectory.

There is also a notable product shift. Younger children reach for bread rolls, pastries, cereal bars. Teenagers go for ready-made sandwiches and hot dogs. There is a pattern here: for children and young people, buying breakfast on the go is a form of autonomy — the ability to make independent purchase decisions, which at this age is becoming an important element of their lives.

What about the rest?

Young adults eat breakfast on the go most frequently. Older groups do so less often and experience greater discomfort. The sense of morning rush increases with age:

18–25: 57% report a rushed morning

26–35: 61%

36–50: 65%

50+: 72% — highest of all groups

At the same time, the 50+ group most often declares having breakfast at home (47%). This is not a contradiction — it is a description of reality: eating at home does not mean a calm morning. It means there is not the time or motivation to go out. For this group, the morning is a task to complete, not a moment to celebrate.

The implication for brands is direct: communicating breakfast convenience through the lens of youth and mobility is only a partially accurate diagnosis. The older part of society is larger, more pressed for time, and spends more. Worth keeping in mind.

What drives the decision — Generational Differences

The definition of a good breakfast differs by generation: for 18–35 — breakfast should not interfere with the morning. For 36–50 — it should provide energy and close out the morning. For 50+ — it should be healthy and make sense.

No single product satisfies all three definitions in the same way. A well-calibrated assortment and segment-specific communication can.u.

The Hot Dog: a shift that has already happened

Back to the starting point: hot dog as breakfast. The scale is large enough that it can no longer be treated as an anomaly.

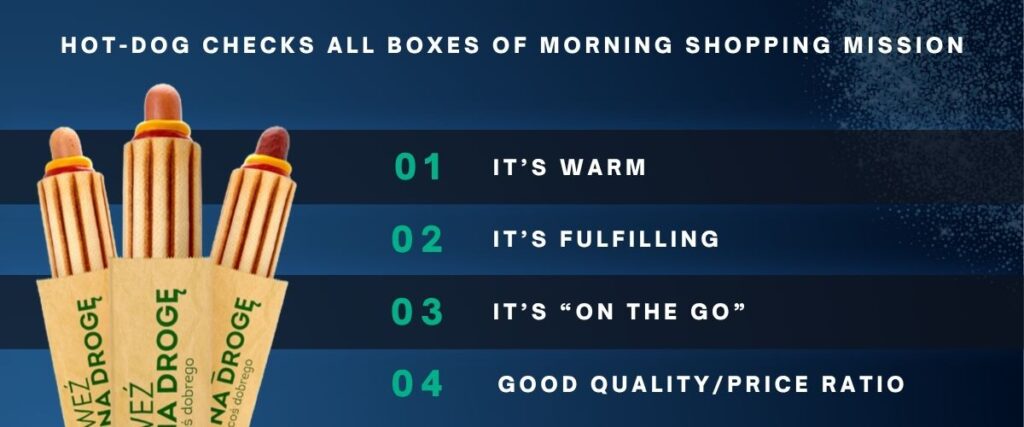

The hot dog satisfies four criteria that matter in the morning purchase mission: it is warm and more filling than a cold bread roll, easy to eat on the move, and has a transparent price-to-satiety ratio.

This means the hot dog operates in two markets simultaneously — adult convenience breakfast and teenage breakfast on the way to school. Brands that communicate it only as a snack are not using the full potential of the purchase mission.

Repositioning from snack to breakfast solution is an important shift in communication context.

What does this mean for brands?

The study points to several things that should change how brands think about the morning breakfast market.

Breakfast has stopped being a meal eaten at home with the family. The majority of Poles — both adults and children — eat their first meal after leaving the house: on the go or immediately upon arriving at work or school. Adults and teenagers buy these breakfasts independently on the way, in the vast majority of cases (home-prepared breakfast is becoming increasingly rare, and applies mainly to the youngest — primary school children).

The common denominator is rush.

From a brand perspective, the most important thing is simplification.

An obvious easy choice, maximum simplicity, a safe familiar product in a familiar form. There is no time for experimentation here.

The brand must fit the consumer’s rhythm.

In marketing terms this means that being present in the convenience channel is not enough. It requires knowing at which moment of the morning the brand needs to act: as the first thought, as a quick suggestion on the route, or as the product that closes the morning mission. The winner is not the one who changes the rhythm, but the one who best fits into the decision that is already about to be made.

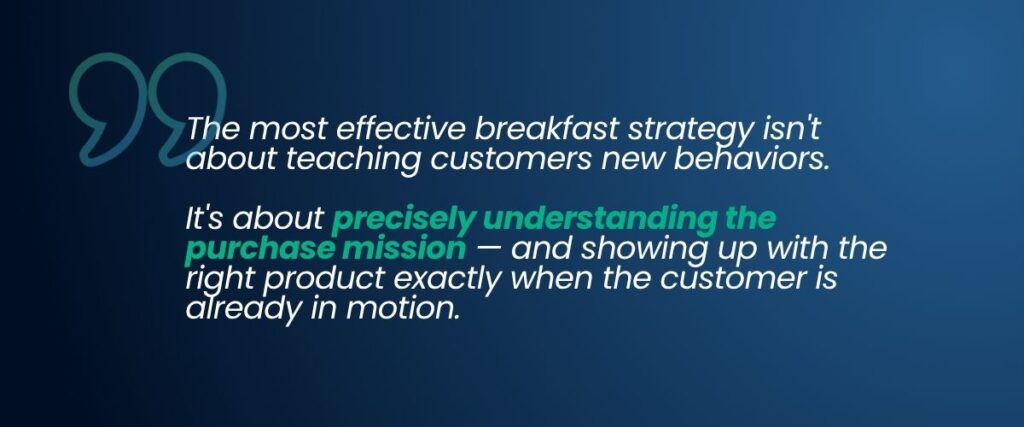

The most effective breakfast strategy is not about teaching customers new behaviors. It is about precisely understanding the purchase mission — and appearing with the right product at exactly the moment the customer is already in motion.

The data that enables this precision — for each segment, in each purchase context — is available. The question is therefore not “whether it is worth having this data,” but “how quickly and effectively we start using it for decisions.”.

Key questions & answers:

How much do Poles spend on breakfast on the go each day?

According to the study of Polish breakfast habits, Poles spend approximately PLN 49.7 million daily on breakfasts consumed outside the home or on the go. The average spend per breakfast is PLN 22, ranging from PLN 18.01 in the 18–25 age group to PLN 25.05 in the 26–35 group.

Why is the hot dog treated as a breakfast solution?

The hot dog satisfies four criteria of the morning purchase mission: it is warm and filling, easy to eat on the move, and has a transparent price-to-satiety ratio. 10% of school-going children buy a hot dog for breakfast. The category therefore functions simultaneously as adult convenience breakfast and as teenagers’ on-the-way-to-school breakfast.

How do breakfast selection criteria differ across generations?

Taste dominates in all groups (41%). But the order of remaining criteria shifts with age: younger groups are more price-sensitive, older groups more health-conscious. The definition of a good breakfast also differs: for 18–35 it should not interfere with the morning; for 36–50 it should provide energy; for 50+ it should be healthy and make sense.

What is a purchase mission and how does it affect breakfast strategy?

A purchase mission describes the goal and context of a store visit. For breakfast on the go the mission is specific and time-constrained: buy something fast, warm or easy to eat before the proper day begins. Understanding the mission — not just the buyer’s demographics — makes it possible to design activations, shelf placement and messaging that fit into the shopper’s natural morning rhythm rather than competing with it.